The Valuation Trap: Oil Price Shock, Inflation, and Record Equity Markets

This blog post touches on the current backdrop surrounding the Iran conflict, recent warnings from IMF Managing Director Kristalina Georgieva and FOMC officials, along with the research of Bill Hester at Hussman Funds, to cover the changing macro regime and its implications for investors.

The S&P 500 touched yet another all-time high as markets enter the seasonally weaker stretch often summarized by the phrase “Sell in May and go away.”

Beneath the surface of this record-breaking rally, however, the macroeconomic backdrop is shifting in ways that deserve far more attention than investors currently appear to be giving it.

In a stark address at the Milken Institute last week, IMF’ chief Georgieva warned that the global economy’s “reference/baseline scenario” — one that assumed a brief, contained conflict in the Middle East, is now firmly in the rearview mirror.

When the U.S.-Iran conflict escalated earlier this year, the IMF’s base case assumed a short conflict with limited economic spillover. That assumption is fading quickly. Georgieva indicated that the IMF is increasingly focused on its adverse scenario, one in which the conflict extends through 2026 and beyond while oil stabilizes closer to $125 per barrel.

The danger for investors is not simply the price of oil.

As Georgieva warned, a prolonged conflict at those high energy prices risks inflation expectations beginning to “de-anchor,” meaning households, businesses, and financial markets stop believing central banks can fully contain inflation and instead begin embedding higher inflation into wages, contracts, and long-term expectations. Once that psychology takes hold, it becomes extremely difficult to reverse.

The International Energy Agency has already described the Strait of Hormuz disruption as one of the most significant oil supply shocks in modern history. Brent crude has climbed above $105 in May, up sharply since the end of 2025, while gasoline prices in the United States continue moving higher.

The Fed: From “Looking Through” to “Leaning In”

The Federal Reserve initially approached the energy spike as a temporary shock it could potentially “look through.” That posture is becoming increasingly difficult to maintain. At the late-April meeting, the Fed held rates steady, but the 8-4 vote (against further easing bias / language) signaledan important internal dissent. The conversation inside the FOMC appears to be shifting from when rate cuts may begin to whether tighter policy could ultimately remain necessary for longer than markets expect.

Large institutional investors are already repricing that reality. Bond markets have steadily reduced expectations for near-term easing as energy-driven inflation risks persist.

PIMCO now places the odds of a rate increase before mid-2027 at nearly 50-50.

Equity Market Valuation Trap

This is where Bill Hester’s January research note becomes especially important.

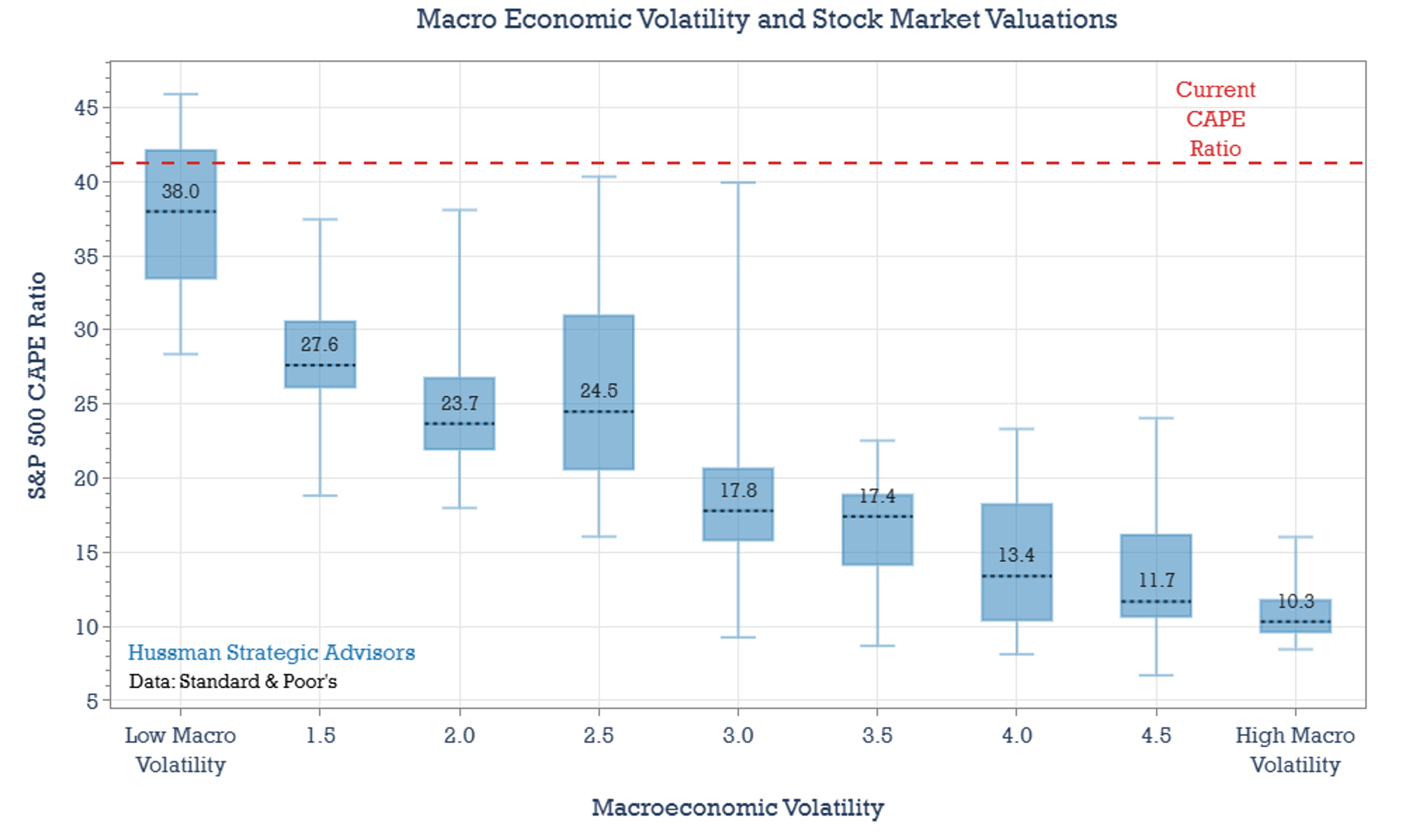

His core argument is that today’s elevated Shiller CAPE ratio — near 41x, roughly double its long-run historical average — only remains sustainable in an environment defined by low and stable inflation, infrequent recessions, and strong confidence in central bank credibility. Remove any one of those pillars, and the valuation math becomes far more difficult to justify.

The research piece highlights the tension between macro volatility and elevated valuations. Historically, when uncertainty rises, investors demand a higher risk premium. In practical terms, that means markets tend to pay lower multiples on future earnings during unstable macro regimes, not higher ones.

Source: Hussmand Funds

History offers a sobering comparison.

The early 1970s also began with elevated valuations and widespread confidence in economic resilience. What followed was not one sudden crash, but a long period of oil shocks, inflation volatility, policy tightening, and repeated recessions that gradually compressed the Shiller P/E ratio from 24 down to 6 over the course of the decade.

The bond market increasingly appears to recognize this risk. Equity markets largely do not.

What This Means for Your Portfolio

None of this guarantees an imminent market collapse. Corporate earnings remain relatively strong, unemployment remains low, and AI-driven productivity gains could continue supporting growth.

But several realities deserve respect:

Valuation matters. In a high-volatility macro regime, richly valued assets become significantly more vulnerable. The “buy the dip” mentality of the last decade was built in an environment of low inflation and abundant central-bank support. That backdrop is changing.

Watch the Strait, not just the Fed. The status of the Strait of Hormuz may now exert more influence on monetary policy than labor-market data alone. A diplomatic resolution could ease pressure quickly, but a prolonged disruption cannot simply be priced away.

Positioning remains stretched. Investor cash allocations remain historically low, leaving relatively little margin for error if macro conditions deteriorate or sentiment shifts abruptly.

The Bottom Line

The “Goldilocks” era of low inflation, low volatility, and a Federal Reserve consistently ready to support markets is under increasing strain. As Bill Hester’s work reminds us, history has rarely been kind to record-high valuations during periods of rising macro instability and persistent energy shocks.

Enjoy the rally while it lasts. Just recognize that discipline, risk management, and valuation awareness may matter far more over the next several years than momentum and optimism alone.